5267

5267  10337

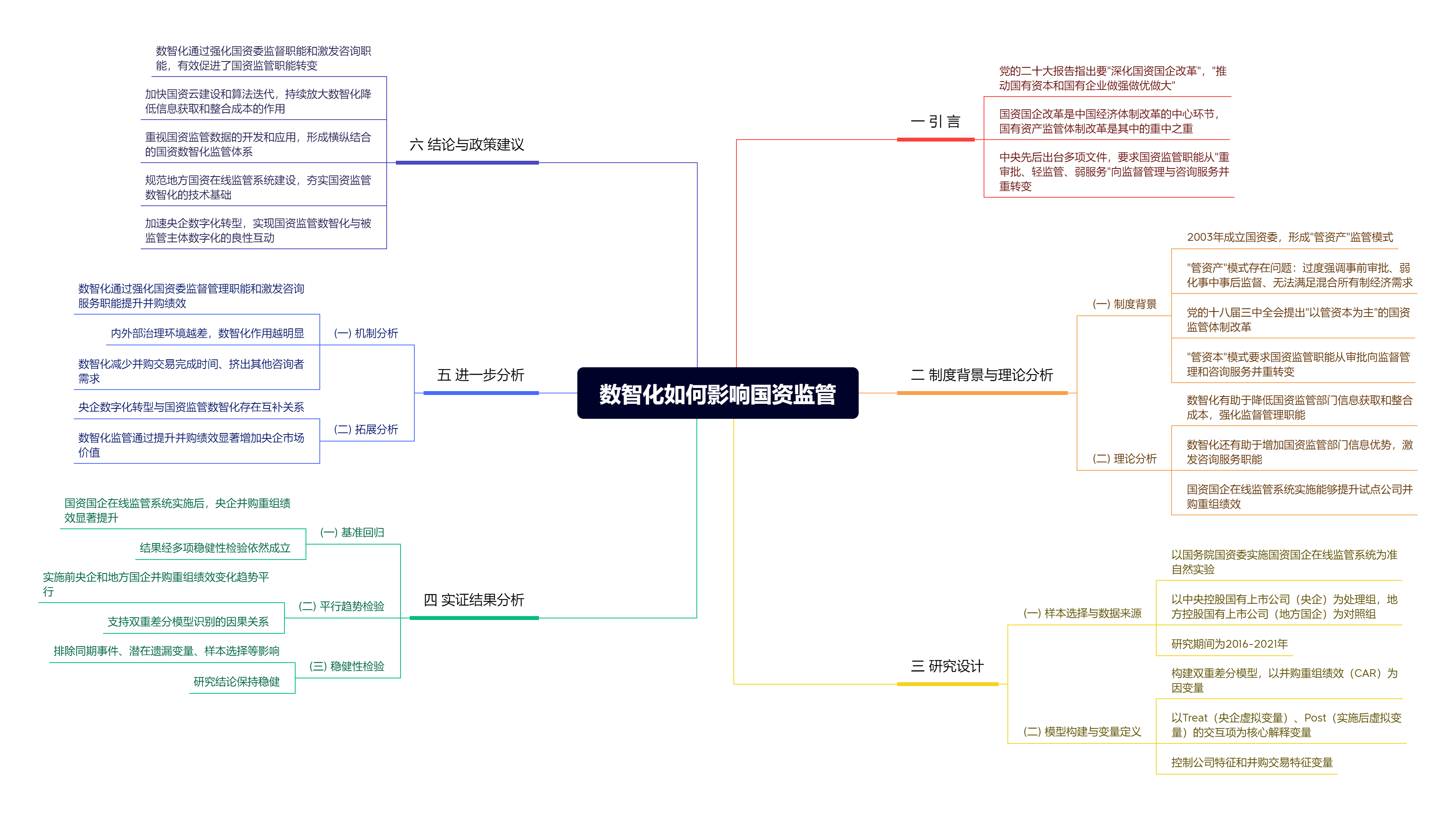

10337促进国资监管从侧重事前审批向兼具监督管理和咨询服务的双重职能转变,是当前国资改革的重中之重。文章以国务院国资委实施国资国企在线监管系统为准自然实验,以2016—2021年国有上市公司发起的并购重组交易为研究对象,采用双重差分模型考察了数智化对国资监管职能转变的作用及其机理。研究发现,在国资国企在线监管系统实施之后,试点公司的并购重组绩效显著提升。强化国资委监督职能和激发国资委咨询职能是数智化监管发挥作用的重要机制,数智化有效促进了国资监管职能转变。数智化监管能够通过提升并购重组绩效,显著增加试点公司的市场价值,助力央企高质量发展。文章的研究揭示了国资国企在线监管系统建设的实际效果,丰富并拓展了数智化监管的相关研究,而且为通过数智化建设来促进国资监管职能转变的政策实践提供了理论参考和完善方向。

数智化如何影响国资监管?——基于国资委监督和咨询双重职能视角的研究

摘要

参考文献

相关附件

思维导图

1 陈冬华,陈信元,万华林. 国有企业中的薪酬管制与在职消费[J]. 经济研究,2005,(2):92−101.

21 Antón M,Azar J,Gine M,et al. Beyond the target:M&A decisions and rival ownership[J]. Journal of Financial Economics,2022,144(1):44−66. DOI:10.1016/j.jfineco.2022.01.002

22 Armstrong C,Kepler J D,Samuels D,et al. Causality redux:The evolution of empirical methods in accounting research and the growth of quasi-experiments[J]. Journal of Accounting and Economics,2022,74(2−3):101521. DOI:10.1016/j.jacceco.2022.101521

23 Bao J,Edmans A. Do investment banks matter for M&A returns?[J]. The Review of Financial Studies,2011,24(7):2286−2315. DOI:10.1093/rfs/hhr014

24 Baron R M,Kenny D A. The moderator–mediator variable distinction in social psychological research:Conceptual,strategic,and statistical considerations[J]. Journal of Personality and Social Psychology,1986,51(6):1173−1182. DOI:10.1037/0022-3514.51.6.1173

25 Beardsley E L,Imdieke A J,Omer T C. The distraction effect of non-audit services on audit quality[J]. Journal of Accounting and Economics,2021,71(2−3):101380. DOI:10.1016/j.jacceco.2020.101380

26 Brooks C,Chen Z,Zeng Y Q. Institutional cross-ownership and corporate strategy:The case of mergers and acquisitions[J]. Journal of Corporate Finance,2018,48:187−216. DOI:10.1016/j.jcorpfin.2017.11.003

27 Brown S J,Warner J B. Using daily stock returns:The case of event studies[J]. Journal of Financial Economics,1985,14(1):3−31. DOI:10.1016/0304-405X(85)90042-X

28 Cai Y,Kim Y,Park J C,et al. Common auditors in M&A transactions[J]. Journal of Accounting and Economics,2016,61(1):77−99. DOI:10.1016/j.jacceco.2015.01.004

29 Chen X,Harford J,Li K. Monitoring:Which institutions matter?[J]. Journal of Financial Economics,2007,86(2):279−305. DOI:10.1016/j.jfineco.2006.09.005

30 Chen Y C,Hung M,Wang Y X. The effect of mandatory CSR disclosure on firm profitability and social externalities:Evidence from China[J]. Journal of Accounting and Economics,2018,65(1):169−190. DOI:10.1016/j.jacceco.2017.11.009

31 Dey A,White J T. Labor mobility and antitakeover provisions[J]. Journal of Accounting and Economics,2021,71(2−3):101388. DOI:10.1016/j.jacceco.2021.101388

32 Frattaroli M. Does protectionist anti-takeover legislation lead to managerial entrenchment?[J]. Journal of Financial Economics,2020,136(1):106−136. DOI:10.1016/j.jfineco.2019.03.014

33 Gokkaya S,Liu X,Stulz R M. Do firms with specialized M&A staff make better acquisitions?[J]. Journal of Financial Economics,2023,147(1):75−105. DOI:10.1016/j.jfineco.2022.09.002

34 Kim Y,Su L X,Zhou G G,et al. PCAOB international inspections and Merger and Acquisition outcomes[J]. Journal of Accounting and Economics,2020,70(1):101318. DOI:10.1016/j.jacceco.2020.101318

35 Laamanen T,Keil T. Performance of serial acquirers:Toward an acquisition program perspective[J]. Strategic Management Journal,2008,29(6):663−672. DOI:10.1002/smj.670

36 Leuz C. Towards a design-based approach to accounting research[J]. Journal of Accounting and Economics,2022,74(2−3):101550. DOI:10.1016/j.jacceco.2022.101550

37 Liu C,Chen Y,Li S M,et al. Local political corruption and M&As[J]. China Economic Review,2021,69:101677. DOI:10.1016/j.chieco.2021.101677

38 Masulis R W,Simsir S A. Deal initiation in mergers and acquisitions[J]. Journal of Financial and Quantitative Analysis,2018,53(6):2389−2430. DOI:10.1017/S0022109018000509

39 Roychowdhury S,Shroff N,Verdi R S. The effects of financial reporting and disclosure on corporate investment:A review[J]. Journal of Accounting and Economics,2019,68(2−3):101246. DOI:10.1016/j.jacceco.2019.101246

本论文包含如下附件:

| 序号 | 标题 | 大小 | 查看/下载 |

|---|---|---|---|

| 1 | 思维导图 | 922.1 (KB) |

引用本文

刘春, 李善民, 孙亮, 等. 数智化如何影响国资监管?——基于国资委监督和咨询双重职能视角的研究[J]. 财经研究, 2024, 50(11): 4-18.

导出参考文献,格式为:

下一篇:证券分析师家乡网络资本的信息效应