9636

9636  18221

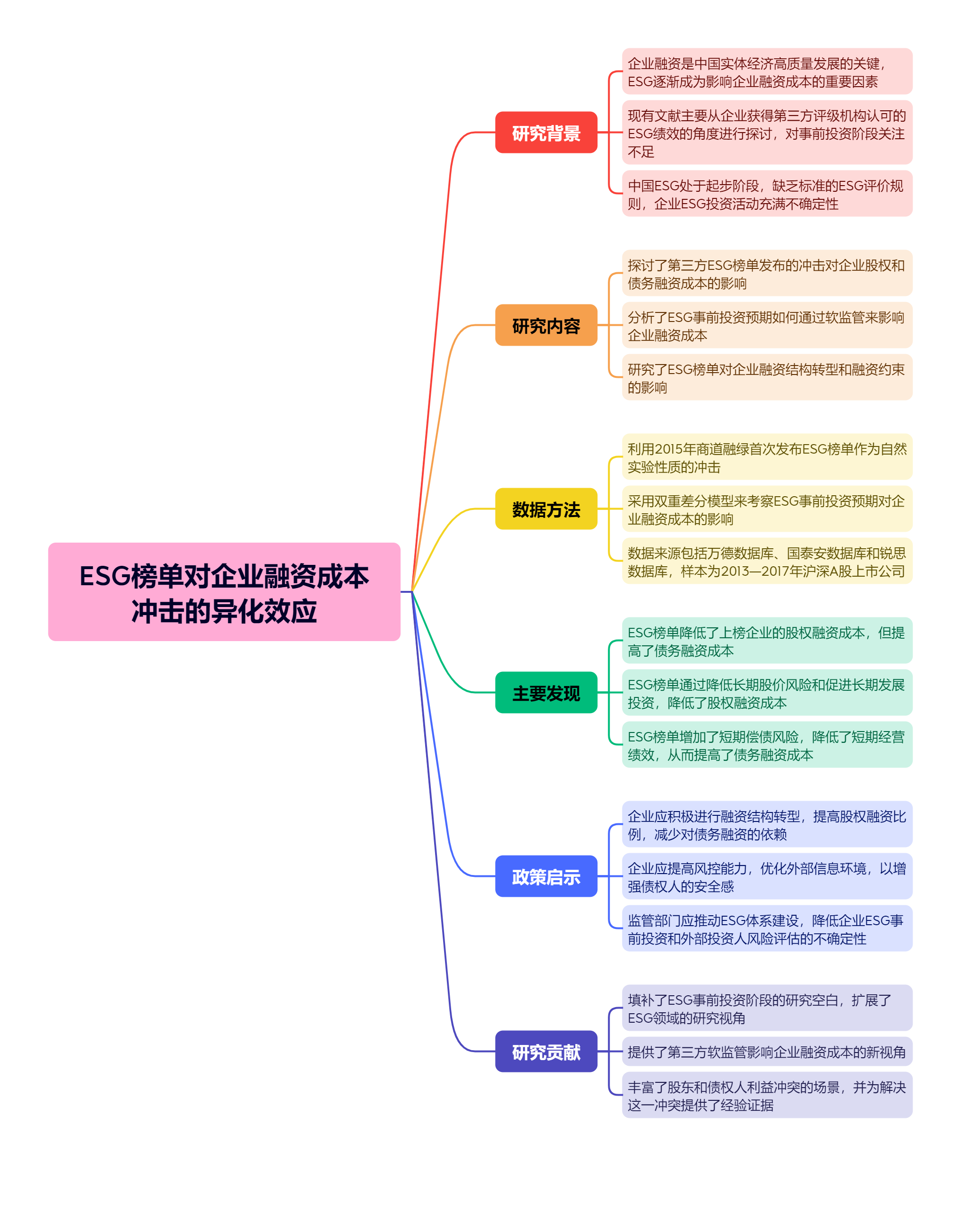

18221与现有文献主要从事后角度探讨ESG绩效的经济后果不同,文章聚焦于ESG事前投资预期如何影响企业融资成本。文章借助2015年商道融绿首次发布ESG榜单这一具有“自然实验”性质的冲击,采用双重差分模型考察了这种软监管所引致的ESG事前投资预期对企业股权和债务融资成本的异化效应及其作用机制。研究表明,由于不同类型投资者的风险偏好和利益导向不同,第三方ESG榜单降低了上榜企业的股权融资成本,但提高了其债务融资成本。作用机制检验表明,ESG榜单通过减小长期股价风险和促进长期发展投资而降低企业的股权融资成本,但通过增加短期偿债风险和降低短期经营绩效而提高债务融资成本。进一步研究发现,风控能力较强和外部信息环境较好的企业不仅能享受ESG榜单冲击所带来的股权融资红利,还能规避债务融资成本方面的负面影响。同时,ESG榜单能够倒逼企业加快融资结构转型,扩大股权融资规模,减少对债务融资的依赖,并整体上改善上榜企业的融资困境。文章填补了ESG事前投资阶段的文献空白,也为ESG中国化实践初期如何协调股东与债权人的利益冲突提供了经验证据。

ESG榜单对企业融资成本冲击的异化效应

摘要

参考文献

相关附件

思维导图

1 陈峻,郑惠琼. 融资约束、客户议价能力与企业社会责任[J]. 会计研究,2020,(8):50−63. DOI:10.3969/j.issn.1003-2886.2020.08.004

26 Broadstock D C,Chan K,Cheng L T W,et al. The role of ESG performance during times of financial crisis:Evidence from COVID-19 in China[J]. Finance Research Letters,2021,38:101716. DOI:10.1016/j.frl.2020.101716

27 Chang X,Chen Y Y,Wang S Q,et al. Credit default swaps and corporate innovation[J]. Journal of Financial Econo- mics,2019,134(2):474−500. DOI:10.1016/j.jfineco.2017.12.012

28 Chen Y C,Hung M Y,Wang Y X. The effect of mandatory CSR disclosure on firm profitability and social externa- lities:Evidence from China[J]. Journal of Accounting and Economics,2018,65(1):169−190. DOI:10.1016/j.jacceco.2017.11.009

29 Christensen D M,Serafeim G,Sikochi A. Why is corporate virtue in the eye of the beholder? The case of ESG ratings[J]. The Accounting Review,2022,97(1):147−175. DOI:10.2308/TAR-2019-0506

30 Da Z,Guo R J,Jagannathan R. CAPM for estimating the cost of equity capital:Interpreting the empirical evidence[J]. Journal of Financial Economics,2012,103(1):204−220. DOI:10.1016/j.jfineco.2011.08.011

31 Easton P D. PE ratios,PEG ratios,and estimating the implied expected rate of return on equity capital[J]. The Accounting Review,2004,79(1):73−95. DOI:10.2308/accr.2004.79.1.73

32 Ee M S,Chao C C,Wang L F S,et al. Environmental corporate social responsibility,firm dynamics and wage inequa- lity[J]. International Review of Economics & Finance,2018,56:63−74.

33 Graham J R,Harvey C R. The theory and practice of corporate finance:Evidence from the field[J]. Journal of Financial Economics,2001,60(2−3):187−243. DOI:10.1016/S0304-405X(01)00044-7

35 Jiang W,Li K,Shao P. When shareholders are creditors:Effects of the simultaneous holding of equity and debt by non-commercial banking institutions[J]. The Review of Financial Studies,2010,23(10):3595−3637. DOI:10.1093/rfs/hhq056

36 Myers S C. Determinants of corporate borrowing[J]. Journal of Financial Economics,1977,5(2):147−175. DOI:10.1016/0304-405X(77)90015-0

37 Ohlson J A,Juettner-Nauroth B E. Expected EPS and EPS growth as determinants of value[J]. Review of Accounting Studies,2005,10(2):349−365.

38 Sandvik J. Board monitoring,director connections,and credit quality[J]. Journal of Corporate Finance,2020,65:101726. DOI:10.1016/j.jcorpfin.2020.101726

39 Zhang A L,Wang S Y,Liu B,et al. How government regulation of interbank financing impacts risk for Chinese commercial banks[J]. Journal of Asian Economics,2020,66:101148. DOI:10.1016/j.asieco.2019.101148

本论文包含如下附件:

| 序号 | 标题 | 大小 | 查看/下载 |

|---|---|---|---|

| 1 | 思维导图 | 681.1 (KB) |

引用本文

刘柏, 卢家锐. ESG榜单对企业融资成本冲击的异化效应[J]. 财经研究, 2024, 50(4): 124-138.

导出参考文献,格式为: